- calendar_month December 21, 2024

- folder Real Estate Tips

Thinking of moving but dreading a steep increase in property taxes? Proposition 19 offers incredible opportunities for California homeowners who are 55 or older, disabled, or affected by wildfires or natural disasters. You can transfer the taxable value of your current home to your new one, potentially saving thousands in property taxes annually!

What is Proposition 19?

Under Proposition 13, passed in 1978, property taxes are based on the purchase price of your home, with a 2% annual increase. This often results in significant tax savings since the average home’s market value typically rises much more than 2% annually. Proposition 19, called The Home Protection for Seniors, Severely Disabled, Families, and Victims of Wildfire or Natural Disasters Act, was approved by voters in 2020 and became effective in 2021. It substantially expanded the ability for certain groups to transfer all or part of their favorable tax basis. Proposition 19 introduced three major changes to the existing law:

- Statewide Flexibility: Proposition 19 allows you to transfer your taxable value to a replacement home in any county in California, eliminating the need for counties to participate in an intercounty transfer program.

- More Transfers: The number of allowable lifetime transfers was increased from one to three.

- Value Limit Removed: Instead of only being able to transfer the tax basis to a home of equal or lesser value, now replacement homes of a higher value are included.

Who qualifies?

The home being sold and the home being purchased must be the homeowner’s primary residence. Three groups of homeowners qualify for the program:

- Any person age 55 or older.

- Any person severely and permanently disabled at any age.

- Victims of a wildfire or Governor-declared disaster whose home was substantially damaged or destroyed. “Substantially damaged” is defined as a loss of over half the market or improvement value.

How Does It Work?

To be considered a primary residence, the original home must be eligible for the either the homeowners' exemption or the disabled veterans' exemption. The replacement dwelling must be eligible for one of the same exemptions at the time it is occupied by the homeowner.

The replacement home must be purchased or constructed within 2 years (before or after) of selling the original home. A claim form must be filed with the county assessor in the county of the replacement home within 3 years after the purchase date, or if new construction, when the construction was completed.

How the tax value is transferred depends on the relative market values of the homes:

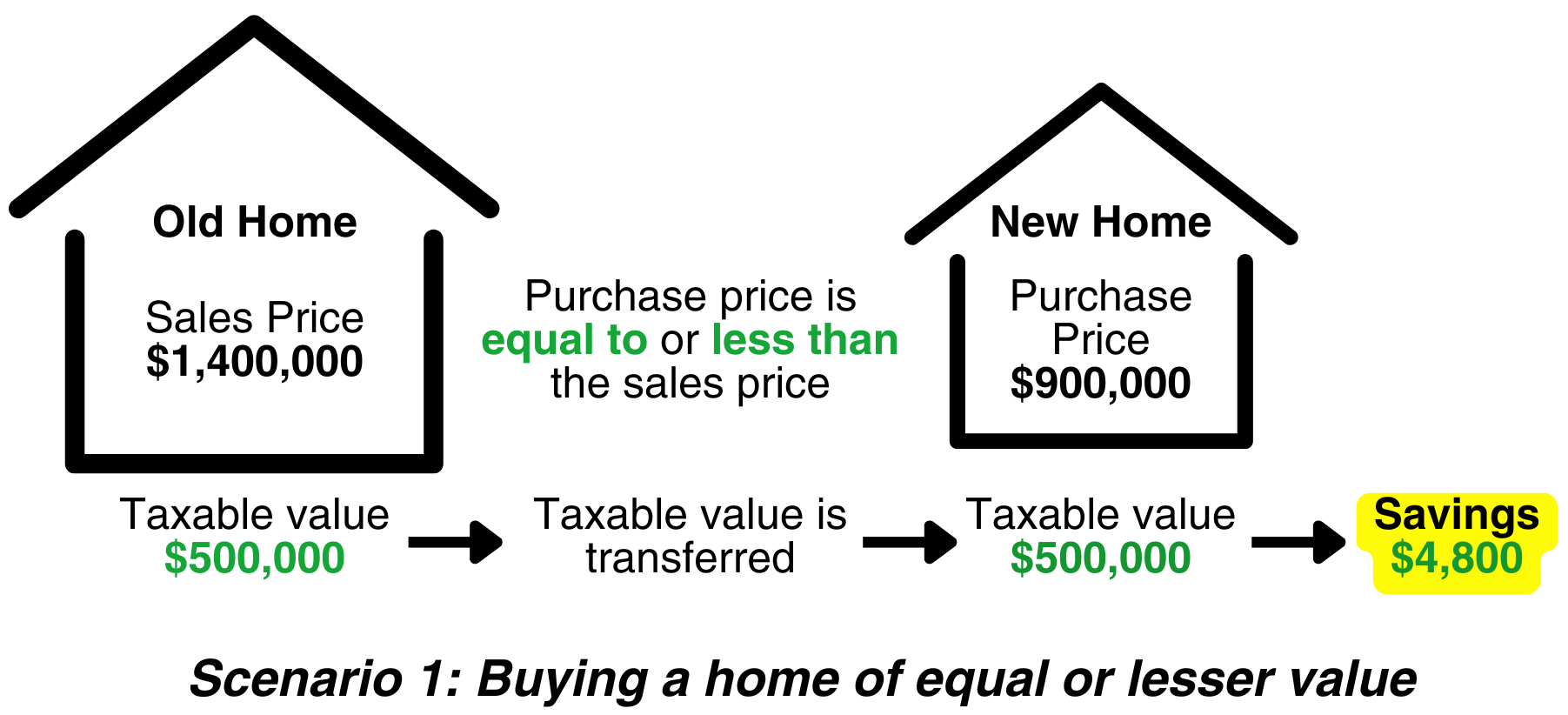

- If your new home’s market value is equal to or less than your old home’s sale price, your original taxable value applies.

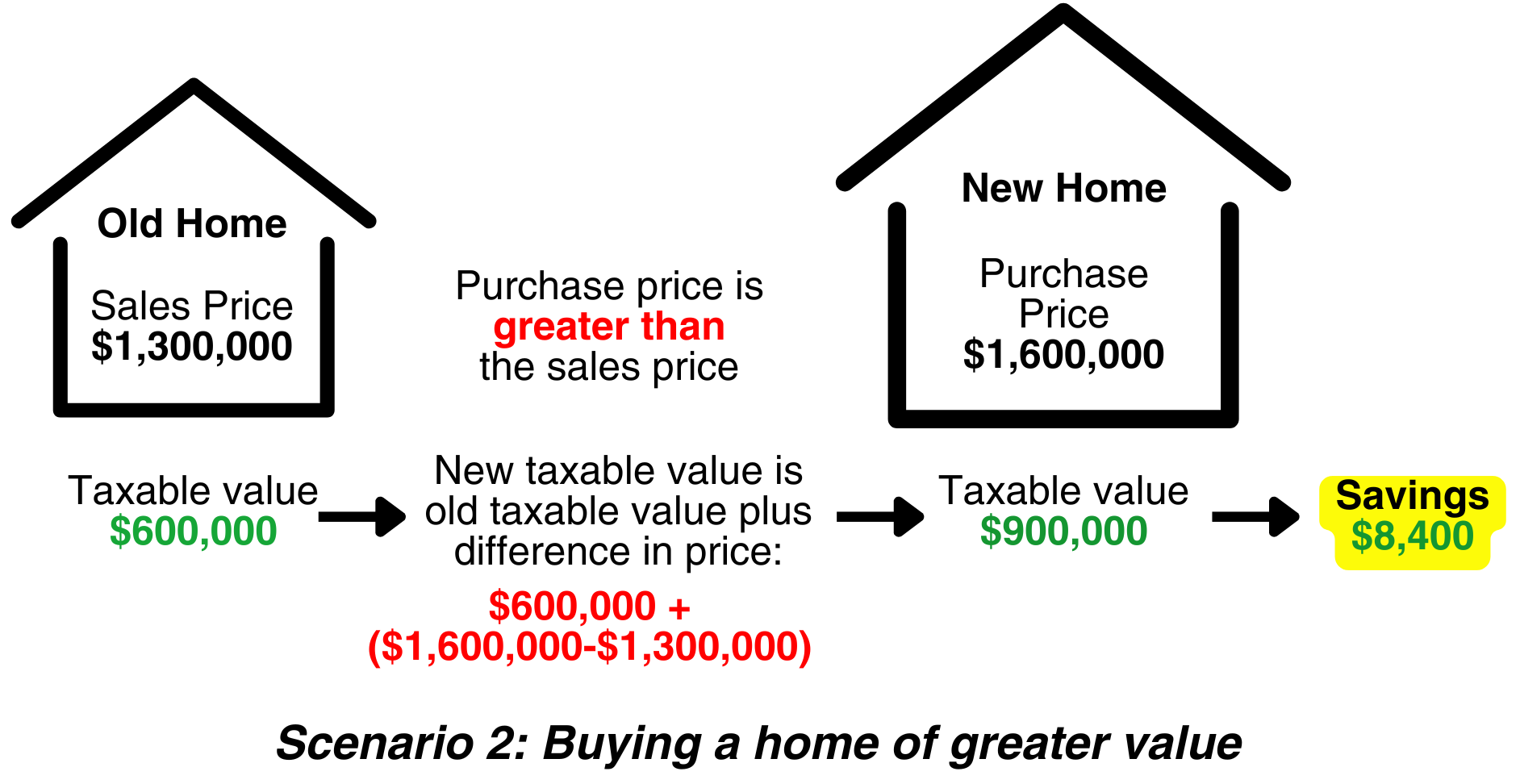

- If your new home’s market value is greater, your taxable value is adjusted by adding the difference in value to the original taxable value.

The replacement home is considered to be of “equal or lesser value” if it is:

- 100% or less of the original home sale price if the replacement home is purchased before the original home is sold.

- 105% or less of the original home sale price if the replacement home is purchased in the first year after sale of the original home.

- 110% or less of the original home sale price if the replacement home is purchased in the second year after sale of the original home.

Some Savings Examples

Here’s how Proposition 19 can save you money:

Scenario 1: You sell your home with a taxable value of $500,000 for $1.4 million and purchase a $900,000 condo. Your taxable value remains $500,000, saving you $4,800 per year, assuming a 1.2% tax rate.

Scenario 2: You sell a home with a taxable value of $600,000 for $1.3 million and buy a $1.6 million property. The new taxable value becomes $900,000 ($600,000 + $300,000 difference), saving you $8,400 annually, assuming a 1.2% tax rate.

Key Points to Remember

A couple things to keep in mind:

- The process is not automatic. You need to obtain and file a form with the assessor in the county where the replacement property is located.

- Be aware of the time limits. Purchase the replacement property within 2 years of selling the original property, and file the assessor form within 3 years after purchasing the replacement property.

Want to dig into more details? Visit the state’s website for Proposition 19, or your local assessor’s office.

Ready to Make Your Next Move?

Let’s explore how Proposition 19 could help you move into your next home without breaking the bank on property taxes. Contact me today for a free consultation!